Investment Property Types

Invest & Earn

7% Net Rent Guaranteed For 5 Years

These investment properties are already rented out to our sub-tenants. They are low cost, give high rental yields and are expected to grow healthily in value over the next few years. They are easy to resell and we continually acquire, sell and sub-let such properties.

All properties within each category are very similar. Rent is 7% and proportional to property price, so you can choose any within your budget. We buy, renovate and categorise them according to their value and investment potential.

2-Bed House

Large

SELLER

£91,999

You buy the property and then rent it directly to us. This system allows you, as the property owner to retain full management control of your property, whilst being a passive investor. These properties are the most popular types with our UK, expat and overseas investors.

Flexi-Furnished

Investment Property

View our investment property types, all associated costs and your guaranteed returns in full detail.

Flexi-Furnished means we can furnish to the needs of our tenants, to maximise our rent and guarantee you a higher net rent of 7% for a minimum of 5 years.

All properties are ‘Type 1 Ownership’ which means they are Freehold or equivalent. You own the property outright. No ground-rent, no service charges and the condition is guaranteed to a good, rentable standard.

H1

Small 2-Bed

£79,999

House Layout

Two small rooms downstairs comprising Lounge and combined Dining Room/Kitchen with rear yard. Two small bedrooms and 3-piece bathroom.

Property Sizes

- Lounge - 12ft by 13ft (3.7m by 4m)

- Kitchen/Diner - 12ft by 10ft (3.7m by 3m)

- Bedroom 1 - 10ft by 13ft (3m by 4m)

- Bedroom 2 - 9ft by 8ft (2.9m by 2.5m)

- Bathroom - 10ft by 6ft (2.9m by 1.9m)

- Rear Yard - Up to 15ft by 13ft (5m by 4m)

- Parking - Free and ample on street

7% Net Rent

£5,600

Per Year

All Costs To Purchase A H1 Property

- £79,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,000 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £84,998

*Non-UK residents pay an additional 2% stamp duty.

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher.

Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H1 Property Examples

This is a real H1 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H2

Standard 2-Bed

£85,999

House Layout

Two rooms downstairs comprising Lounge and combined Dining Room/Kitchen with rear yard and two bedrooms upstairs, plus a 3-piece bathroom.

Property Sizes

- Lounge - 12ft by 13ft (3.7m by 4m)

- Kitchen/Diner - 12ft by 13ft (3.7m by 4m)

- Bedroom 1 - 14ft by 13ft (3m by 4m)

- Bedroom 2 - 11ft by 8ft (3.4m by 2.5m)

- Bathroom - 10ft by 7ft (3m by 2.1m)

- Rear Yard- Up to 20ft by 13ft (6m by 4m)

- Parking - Free and ample on street

7% Net Rent

£6,020

Per Year

All Costs To Purchase A H2 Property

- £85,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,300 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £91,298

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H2 Property Examples

This is a real H2 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H3 (BEST SELLER)

Large 2-Bed

£91,999

House Layout

Three rooms downstairs (Lounge 1, Lounge 2, Dining Room and separate Kitchen with rear yard. Two bedrooms upstairs plus 3-piece bathroom.

Clients normally make a reservation of this “Best Buy” H3 Type initially. They are free to upgrade or downgrade at the selection stage.

Property Sizes

- Lounge 1 - 14ft by 13ft (4.3m by 4m)

- Lounge 2 - 12ft by 13ft (3.7m by 4m)

- Kitchen/Diner - 8ft by 6ft (2.5m by 1.9m)

- Bedroom 1 - 14ft by 13ft (3m by 4m)

- Bedroom 2 - 11ft by 8ft (3.4m by 2.5m)

- Bathroom - 10ft by 7ft (3m by 2.1m)

- Rear Yard- Up to 20ft by 13ft (6m by 4m)

- Car Parking - Free and ample on street

7% Net Rent

£6,440

Per Year

All Costs To Purchase A H3 Property

- £91,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,600 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £97,598

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

SELLER

H3 Property Examples

This is a real H3 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H4

Small 3-Bed

£92,999

House Layout

Three rooms downstairs comprising Lounge 1, Lounge 2 and combined Dining Room/Kitchen. Rear yard and three bedrooms upstairs, plus a 3-piece bathroom.

Property Sizes

- Lounge 1 - 14ft by 13ft (4.3m by 4m)

- Lounge 2 - 12ft by 13ft (3.7m by 4m)

- Kitchen/Diner - 12ft by 13ft (3.7m by 4m)

- Bedroom 1 - 14ft by 13ft (3m by 4m)

- Bedroom 2 - 11ft by 8ft (3.4m by 2.5m)

- Bedroom 3 - 11ft by 8ft (3.4m by 2.5m)

- Bathroom - 10ft by 7ft (3m by 2.1m)

- Rear Yard- Up to 20ft by 13ft (6m by 4m)

- Parking - Free and ample on street

7% Net Rent

£6,510

Per Year

All Costs To Purchase A H4 Property

- £92,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,650 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £98,648

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H4 Property Examples

This is a real H4 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H5

Large 3-Bed

£98,999

House Layout

Three rooms downstairs. Lounge, Lounge/Dining Room and separate Kitchen. Rear yard and three bedrooms upstairs plus 3-piece bathroom.

Property Sizes

- Lounge 1 - 14ft by 13ft (4.3m by 4m)

- Lounge/Diner - 14ft by 13ft (4.3m by 4m)

- Kitchen - 8ft by 6ft (2.5m by 1.9m)

- Bedroom 1 - 14ft by 13ft (3m by 4m)

- Bedroom 2 - 11ft by 8ft (3.4m by 2.5m)

- Bedroom 3 - 10ft by 8ft (3m by 2.5m)

- Bathroom - 10ft by 7ft (3m by 2.1m)

- Rear Yard - Up to 20ft by 13ft (6m by 4m)

- Parking - Free and ample on street

7% Net Rent

£6,930

Per Year

All Costs To Purchase A H5 Property

- £98,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,950 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £104,948

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H5 Property Examples

This is a real H5 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H6

3-Bed & Garden

£106,999

House Layout

Three rooms downstairs comprising Lounge 1, Lounge 2 and combined Dining Room/Kitchen. Three bedrooms upstairs with a 3-piece bathroom. Front and Rear Garden.

Property Sizes

- Large Lounge (some with 2 lounges)

- Dining Kitchen

- Bedroom 1

- Bedroom 2

- Bedroom 3

- Bathroom

- Front & Rear Garden

- Parking - Free and ample on street

7% Net Rent

£7,490

Per Year

All Costs To Purchase A H6 Property

- £106,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £5,350 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £113,348

*Non-UK residents pay an additional 2% stamp duty.

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher.

Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H6 Property Examples

This is a real H6 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H7

2-Bed Semi-Detached

£115,999

House Layout

Semi-Detached are our most expensive houses. They have a more modern design and plenty of space at the front and large rear gardens.

Property Features

- Large Lounge (some with 2 lounges)

- Dining Kitchen

- Bedroom 1

- Bedroom 2

- Bathroom

- Front & Rear Gardens

- Car Parking Off Road x1

7% Net Rent

£8,120

Per Year

All Costs To Purchase A H7 Property

- £115,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £5,800 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £122,798

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H7 Property Examples

This is a real H7 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H8

3-Bed Semi-Detached

£128,999

House Layout

Semi-Detached are the most expensive but represent great value with good capital growth potential. They have a more modern design and plenty of space at the front and large rear gardens, and are extremely popular in the rental market.

Property Features

7% Net Rent

£9,030

Per Year

- Large Lounge (some with 2 lounges)

- Dining Kitchen

- Bedroom 1

- Bedroom 2

- Bedroom 3

- Bathroom

- Front & Rear Gardens

- Car Parking Off Road x2

All Costs To Purchase A H8 Property

- £128,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £6,450 Stamp Duty @ 5% (Applicable if you already own another property)

Total Cost £136,448

*Non-UK residents pay an additional 2% stamp duty.

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher.

Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H8 Property Examples

This is a real H8 Property Listing which we have recently sold.

Learn more about Our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H1

Small 2-Bed

£79,999

House Layout

Two small rooms downstairs comprising Lounge and combined Dining room/Kitchen with rear yard. Two small bedrooms and 3-piece bathroom.

Property Sizes

- Lounge - 3.7m x 4m

- Kitchen/Diner - 3.7m x 3m

- Bedroom 1 - 3m x 4m

- Bedroom 2 - 2.9m x 2.5m

- Bathroom - 2.9m x 1.9m

- Rear Yard - Up to 5m x 4m

- Parking - Free/ample on street

All Costs To Purchase A H1 Property

- £79,999 Property Price

-

£999 Purchase Cost

(Solicitor, land registry, local searches and 1 yr insurance) -

£4,000 Stamp Duty @ 5%*

(Applicable if you already own another property)

Total Cost £84,998

*Non-UK residents pay an additional 2% stamp duty.

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher.

Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H1 Property Examples

This is a real H1 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H2

Standard 2-Bed

£85,999

House Layout

Two rooms downstairs comprising Lounge and combined Dining Room/Kitchen with rear yard and two bedrooms upstairs, plus a 3-piece bathroom.

Property Sizes

Per Year

- Lounge - 4.3m x 4m

- Kitchen/Diner - 3.7m x 4m

- Bedroom 1 - 3m x 4m

- Bedroom 2 - 3.4m x 5m

- Bathroom - 3m x 2.1m

- Rear yard - Up to 6m x 4m

- Parking - Free/ample on street

All Costs To Purchase A H2 Property

- £85,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,300 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £91,298

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H2 Property Examples

This is a real H2 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H3 (BEST SELLER)

Large 2-Bed

£91,999

BEST

SELLER

House Layout

Property Sizes

- Lounge 1 - 4.3m x 4m

- Lounge 2 - 3.7m x 4m

- Kitchen/Diner - 2.5m x 1.9m

- Bedroom 1 - 3m x 4m

- Bedroom 2 - 3.4m x 2.5m

- Bathroom - 3m x 2.1m

- Rear Yard - Up to 6m x 4m

- Parking - Free/ample on street

All Costs To Purchase A H3 Property

- £91,999 Property Price

-

£999 Purchase Cost

(Solicitor, land registry, local searches and 1 yr insurance) -

£4,600 Stamp Duty @ 5%*

(Applicable if you already own another property)

Total Cost £97,598

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H3 Property Examples

This is a real H3 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H4

Small 3-Bed

£92,999

House Layout

Property Sizes

- Lounge 1 - 4.3m x 4m

- Lounge 2 - 3.7m x 4m

- Kitchen/Diner - 3.7m x 4m

- Bedroom 1 - 3m by 4m

- Bedroom 2 - 3.4m x 2.5m

- Bedroom 3 - 3.4m by 2.5m

- Bathroom - 3m x 2.1m

- Rear Yard - Up to 6m x 4m

- Parking - Free/ample on street

Per Year

All Costs To Purchase A H4 Property

- £92,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £4,650 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £98,648

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H4 Property Examples

This is a real H4 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H5

Large 3-Bed

£98,999

House Layout

Property Sizes

- Lounge 1 - 4.3m x 4m

- Lounge/Diner - 4.3m x 4m

- Kitchen - 2.5m x 1.9m

- Bedroom 1 - 3m x 4m

- Bedroom 2 - 3.4m x 2.5m

- Bedroom 3 - 3m x 2.5m

- Bathroom - 3m x 2.1m

- Rear Yard - Up to 6m x 4m

- Parking - Free/ample on street

Per Year

All Costs To Purchase A H5 Property

- £98,999 Property Price

-

£999 Purchase Cost

(Solicitor, land registry, local searches and 1 yr insurance) -

£4,950 Stamp Duty @ 5%*

(Applicable if you already own another property)

Total Cost £104,948

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H5 Property Examples

This is a real H5 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H6

3-Bed & Garden

£106,999

House Layout

Property Sizes

Per Year

- Large Lounge (some x2 )

- Dining Kitchen

- Bedroom 1

- Bedroom 2

- Bedroom 3

- Bathroom

- Front/Rear Garden

- Parking - Free/ample on street

All Costs To Purchase A H6 Property

- £106,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £5,350 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £113,348

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H6 Property Examples

This is a real H6 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H7

2-Bed

Semi-Detached

£115,999

House Layout

Semi-Detached are our most expensive houses. They have a more modern design and plenty of space at the front and large rear gardens.

Property Sizes

Per Year

- Large Lounge (some x2)

- Dining Kitchen

- Bedroom 1

- Bedroom 2

- Bathroom

- Front & Rear Gardens

- Car Parking Off Road x1

All Costs To Purchase A H7 Property

- £115,999 Property Price

-

£999 Purchase Cost

(Solicitor, land registry, local searches and 1 yr insurance) -

£5,800 Stamp Duty @ 5%*

(Applicable if you already own another property)

Total Cost £122,798

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H7 Property Examples

This is a real H7 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

H8

3-Bed

Semi-Detached

£128,999

House Layout

Property Sizes

Per Year

- Large Lounge (some x2)

- Dining Kitchen

- Bedroom 1

- Bedroom 2

- Bedroom 3

- Bathroom

- Front & Rear Gardens

- Car Parking Off Road x2

All Costs To Purchase A H8 Property

- £128,999 Property Price

- £999 Purchase Cost (Solicitor, land registry, local searches and 1 yr insurance)

- £6,450 Stamp Duty @ 5%* (Applicable if you already own another property)

Total Cost £136,448

Unfurnished properties cost £6k – £8k less and pay 6% net rent for a minimum of 3 years.

Prices shown are for our standard houses in the North East.

North West prices are £10,000 extra and rent is proportionately higher. Pay Total Cost above to own fully. No other costs other than those stated above.

Pay £3,000 at initial reservation. Rest at completion of purchase (minus the £3,000).

H8 Property Examples

This is a real H8 Property Listing which we have recently sold.

Learn more about our Reserve & Select System.

We Take Care Of All

Landlord Liabilities

Annual Gas & Electrical Certificates

All Repairs & Tenant Damage

Council Tax & Any Other Bills If Empty

All Other Liabilities

You Remain The Passive Owner

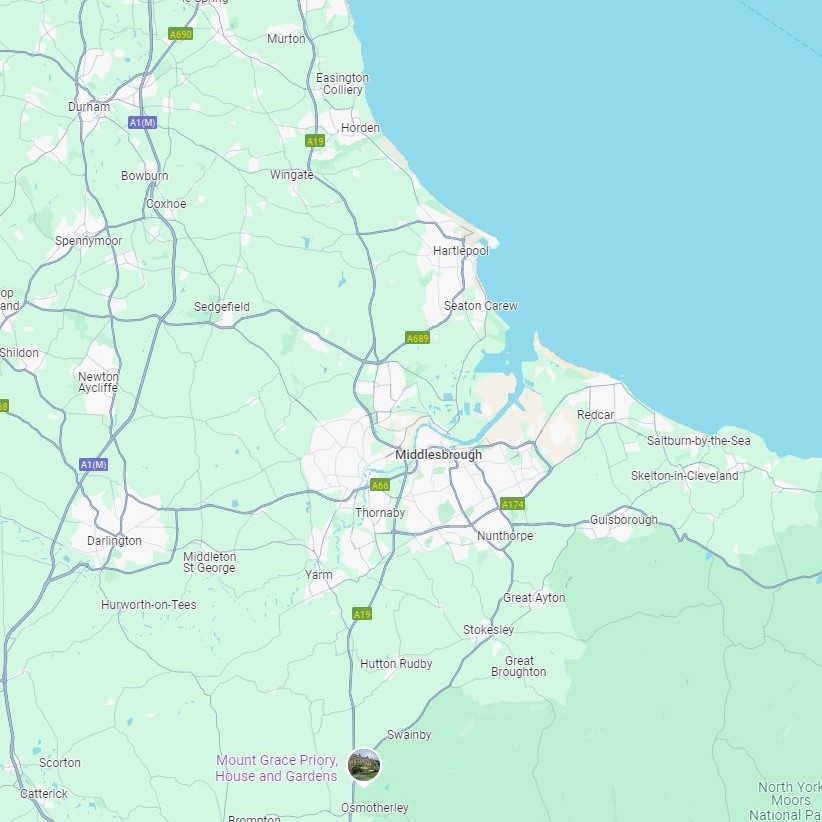

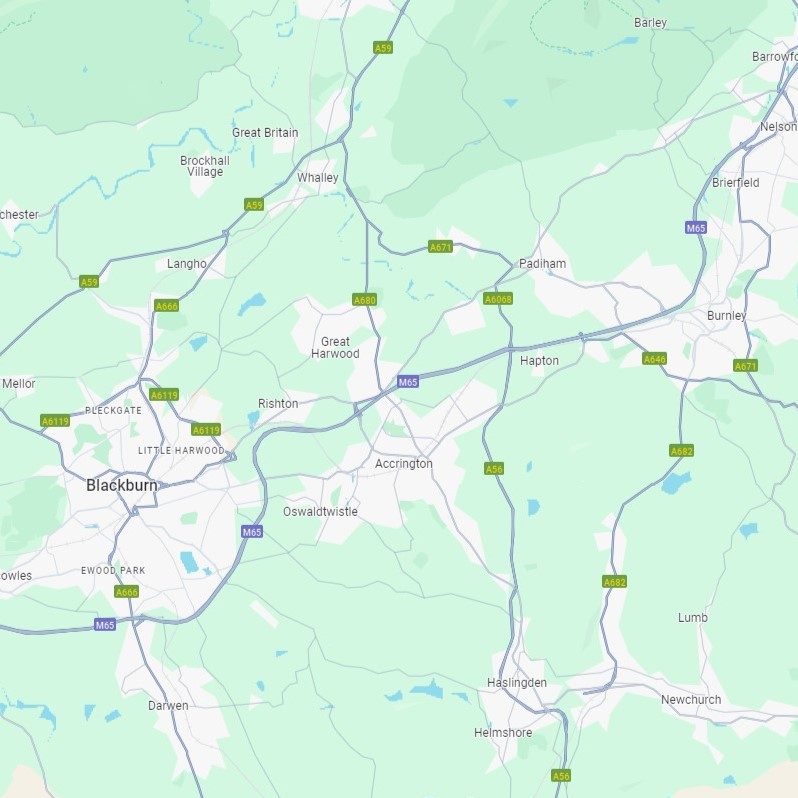

Our Property Locations

North East England

County Durham, Tyne & Wear and North Yorkshire

North West England

Lancashire

Our Property Buying Process

- 10 Easy Steps

- Quick and Low Cost

- Contractually Guaranteed

- Fully Managed

How We Renovate Your Property

- Featured on the BBC

- Homes Under The Hammer

- 7 Episodes